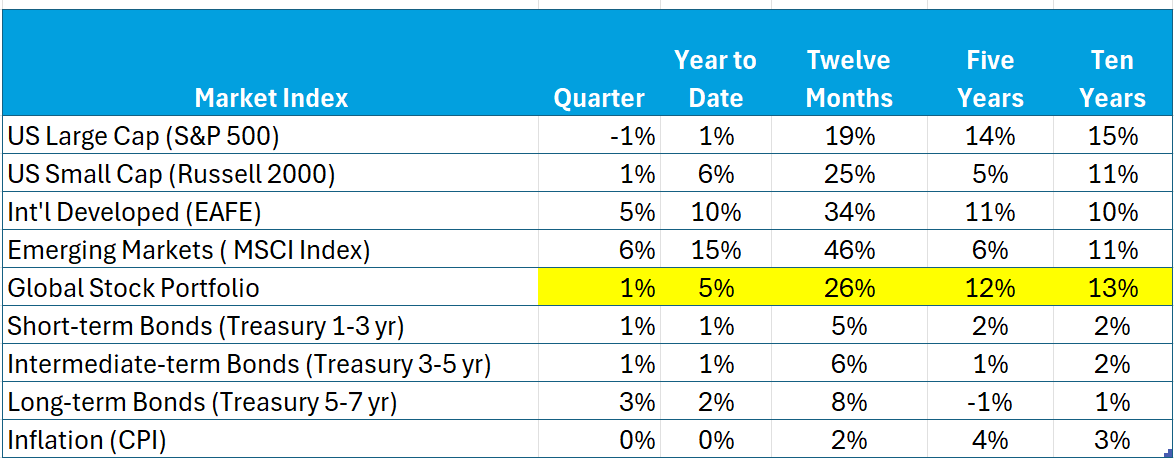

Except for the AI-dominated S&P 500 index, stocks continue to move ahead across a broad front. Bonds reflect a slight drop in longer-term yields. Here’s the data for several periods ending February:

Stocks

Except for the S&P 500, stock market indices continued their positive trajectory in February. The S&P 500 reported above is a capitalization-weighted index – the largest companies have a greater impact on results. An equally weighted S&P 500 index was up 3%, well above what’s reported above, which indicates not only the positive contribution of non-tech, sometimes called HALO (heavy assets, low- obsolescence) stocks, but also the drag from AI stocks. Additionally, returns in both domestic small cap markets and especially international markets were positive. February’s results confirm the value of diversification.

Look at the returns from equity market indices over 10 years, well above the CPI. A nice period for stocks.

Not surprisingly, the Supreme Court ruled that the International Emergency Economic Powers Act (IEEPA) did not give the President authorization to unilaterally implement tariffs. Yet not only does the Administration continue to look for other legal authorities to implement its tariff policy (whatever that is), it also is not clear how to “refund” tariffs that have been collected illegally. Adding to the worldwide uncertainty is the recent attack on Iran. We can expect continued market volatility.

Value of the dollar continued to decline in February, reflecting political uncertainties and helping to explain positive results of international markets.

Bonds

Bond returns were slightly positive, reflecting a drop in yields, especially at the longer end.

While global stocks provided inflation-adjusted (real) returns in all periods, bonds, except for the past year, did not. However, this result will not always be the case, and a commitment to bonds will reduce variability (risk) of a diversified portfolio over longer periods.

Except for the five-year period, which reflects government response to and supply chain disruptions from the Pandemic, inflation is in check. The spread between nominal and inflation-adjusted yields, a reasonable measure of inflation expectations, has remained virtually constant at just above 2% – not far from the Fed’s target.

Risk-Aversion

The Magnificent Seven portfolio, a good proxy for the market’s valuation of AI, is off 8% from the first of the year. This pause is evidence of the risk of this portfolio. It may be useful to look at its behavior in the recent past for insight into its risk and future expectations.

The Magnificent Seven portfolio earned an average monthly return of 3% with a standard deviation of 9%, over the recent eight years, a period that has included the introduction of transformative and uncertain AI technology. This standard deviation is well above the comparable 5% standard deviation of the S&P 500. Clearly riskier. This comparison is understated because the index is heavily weighted (37%) to the Magnificent Seven.

There is clearly significant variability in the value of the Magnificent Seven portfolio. Consequently, the ups and downs we observe, including any “correction,” reflect the risk associated with the market pricing of the vastly uncertain future of AI.