The month of April brought back investors’ appetite for risk. Capital markets seemed to have shrugged off the Middle East turmoil as stocks soared. Here’s the data:

Stocks

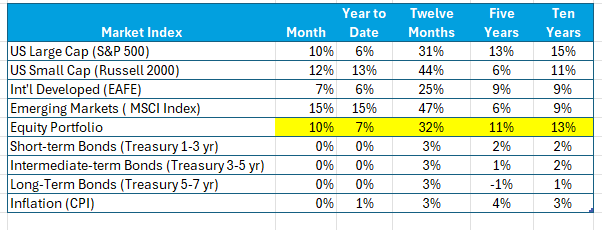

Stocks snapped back in April. The S&P 500, led by the Magnificent Seven, was up 10%. The riskier markets – Russell 2000 and Emerging Markets indices – were up 12% and 15%, respectively. The Emerging Markets index was led by South Korea (up 32%) and Taiwan (up 27%). These results reflect renewed enthusiasm for technology primarily. Stock markets continue to be volatile, moving with the latest news from the Middle East.

Look at the stock results over the past twelve months – truly extraordinary – and reflect a bounce from April 2025, when the announcement of tariffs produced a sharp sell-off. Additionally, these results simply bring the five-year returns closer to long-term averages due to negative returns in 2022. This variability in recent annual returns confirms the need to avoid extrapolating short-term results, either positive or negative.

The price is the present value of future cash flows, which come from company profits. Companies are reporting a significant uptick in first-quarter profits, which helps explain the positive stock results.

Bonds

April bond returns are essentially flat due to a slight uptick in nominal bond yields, due to increasing inflation expectations. The difference between nominal and inflation-adjusted yields (a reasonable measure of market’s expected inflation over the period) at five-year maturity is 2.7% versus 2.6% last month.

A new Chair of the Fed, Kevin Warsh, seems ready to replace Powell. During his confirmation hearing Warsh said all the right things about Fed independence. Yet, remaining free of political interference in today’s environment brings challenges and uncertainty. Current signals from the Fed are for little change in interest rates, with any bias being on the upside.

Inflation

While inflation can result from “too much money chasing too few goods,” due to deficits or lax monetary policy, the current concern is rising prices from a spike in energy costs due to the shutting of the Gulf of Hormuz. This “cost push” inflation can be transitory unless expected inflation gets factored into pricing decisions. Should that happen, inflation can become self-fulfilling.

Inflation measures the rate of change in price levels, which are a snapshot of the costs of a basket of goods and services. A 2% inflation rate (current Fed target) means that at the end of five years we are paying about 10% more for this basket. Unless incomes keep up, consumers fall behind. Inflation distorts economic activity and produces angry consumers.

A bout of inflation in the short term due to supply constraints seems reasonable. However, current bond yields anticipate longer-term inflation of 3%. While above Fed targets and what we have been used to, it provides some perspective on today’s inflation noise. We’ll see.

Today’s Investment Environment

Plenty of uncertainty remains – the status of the Iran War and its impact on the Strait of Hormuz, inflation, changes at the Fed, and political dysfunction are examples. Consequently, the current renewed appetite for risk may be misplaced. Regardless, markets will remain volatile.