Making the Case for International Exposure

“Why would I invest in anything other than the S&P 500 if it continues to do so well?” This is a question that is commonly asked by many of our clients over the past few years. To truly optimize your portfolio and ensure you’re not missing out on potential opportunities, it’s crucial to understand the […]

Rockbridge Institutional – December 2022 Market Review

2022 in the Rear View Mirror Inflation, the Fed’s response and rising interest rates, a sharp falloff in stock and bond prices, uncertainty of a looming recession and Cryptocurrency implosion were all part of the investment landscape in 2022. Although we don’t know what’s ahead, glad this year is behind us. Inflation and Interest Rates […]

Rockbridge Institutional – November 2022 Market Review

MARKET COMMENTARY Stocks After this week’s ups and downs, stocks ended November up nicely – international and emerging market stocks leading the way earning 11% and 15%, respectively. While not as robust, domestic large cap markets were up 6% and small-company markets returned 2%. These results bring the quarter-to-date returns to 14% for domestic markets, […]

Rockbridge Institutional – October 2022 Market Review

MARKET COMMENTARY Stocks Except for emerging markets, stocks were up in October. Domestic markets led the way – large cap (S&P 500) up 9%; small cap (Russell 2000) up 11%. International developed markets (EAFE Index) were up 5%, while emerging markets (MSCI Index) were off 3% due to sharply negative results in China. While uncertainty […]

Capital Market Activity (September, 2022)

August saw significant up and downs in stock returns. In the first half of the month a global stock portfolio was up about 3%, then dropped 6% to a loss of almost 3% after Fed Chairman Powell publicly reaffirm its commitment to increasing interest rates until inflation is in check. Domestic large cap equities were […]

Inflation Commentary (August, 2022)

The Consumer Price Index (CPI) climbed to a historically high 9% over the past twelve months prompting concerns for ongoing inflation. There is much discussion in the popular press as to the causes and to the extent it is “transitory” or is becoming embedded in economic activity. While the emergence of inflation contributes to market […]

Capital Market Activity (August, 2022)

After a sharp decline in the first six months of this year, stocks were up nicely in July; a global equity portfolio was up just over 6%. These results were a welcome respite from what we have experienced thus far this year. Markets look to the future. Let us hope they signal positive expectations for […]

Capital Market Activity – 05/31/2022

Stock Markets Although rebounding lately, all markets are down year to date. Since December stock markets are off more than 10%. Tech stocks are especially hard hit – an equally weighted portfolio of the largest domestic tech stocks (Apple, Microsoft, Amazon, Google, and Facebook) is off 25%. The premium to value markets, domestic and international, […]

Major Firms predict Expected Returns in the coming Decade

Every year large Wall Street firms publish their forecast of expected returns for the coming decade. The following table shows what each firm expects from capital markets in the coming 10-years. The first thing that jumps out is the poor expected performance by U.S. equities. Despite averaging nearly 10% over the last 100 years, forecasters […]

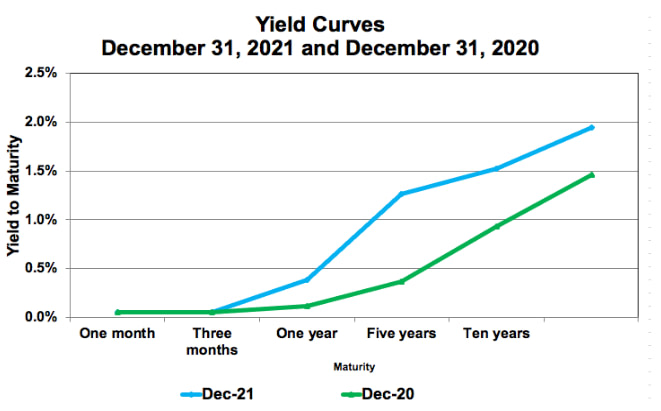

Market Commentary: Q4 2021

2021 was a good year for domestic stocks, with large-cap stocks (S&P500) up 29%. Returns in this market segment continue to be driven by the largest tech stocks, which had been the case for the last ten years. Results in other markets are mixed.REITs produced extraordinary returns bouncing back from last year’s sharp fall-off. Emerging […]