Continuing to shrug off political and economic uncertainty, stocks pushed ahead in May. Bond yields are up a bit. Here’s the data:

Stocks

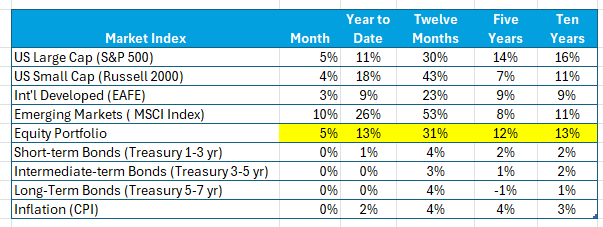

Stock results are consistent with an ongoing willingness to accept risk. Continued enthusiasm for the expected payoff from investments in AI technology explains May’s positive results for the S&P 500 and Emerging Markets Index. Returns for the Magnificent Seven (Amazon, Apple, Google, Meta, Microsoft, Nvidia, Tesla) were up an average of 5.5% in May.

The extraordinary result in Emerging Markets (up 10% in May and a remarkable 53% over the past twelve months) is explained primarily by what’s happening in just three technology companies (TSMS [Taiwan market], SK-Hynix and Samsung [South Korea Market]), which account for over 40% of the market in each of two countries. The results of Taiwan and South Korea indices explain virtually 100% of the year-to-date results of our Emerging Markets index.

Stocks have rewarded investors in recent periods. Returns from all our stock market indices and our global portfolio are at or above long-term averages. The past twelve months’ returns are extraordinary. However, as the warning the SEC requires on investment advertisements tell us: “past results are not indicative of future performance.”

Bonds

Yields were flat in May but increased year-to-date. The yield on the 10-year bellwether Treasury is up 0.08% last month and 0.3% since the beginning of the year.

The Consumer Price Index (CPI) is up 4% since January, well above the Fed goal. However, expected future inflation that’s reflected in five- and ten-year bond yields, while up a bit this month, has remained relatively constant.

Today’s Investment Environment

We are surrounded by uncertainty. Examples include not only the potential payoff from AI investments, but also energy and food inflation, Fed policies, market volatility and valuations, political dysfunction, foreign policy, a credit bubble, deficits and a potential recession. Yet, stock markets continue to surge forward.

Much of the expected value from AI is concentrated in just a few companies. The Magnificent Seven companies have added over $9.0 trillion in value over the last three years – over one-half from Nvidia alone. (Micron, hard at work establishing its headquarters and manufacturing operations in Syracuse, while not part of the “Magnificent Seven,” joined the $1.0 trillion club in May). The three Taiwanese and South Korean emerging market companies noted above have added nearly $3.0 trillion in market value over this period as well. To paraphrase Everett Dirksen (a well-known senator of two generations ago) “a trillion here, a trillion there, pretty soon you’re talking real money!” Truly, an extraordinary period.

These massive amounts of capital attributable to AI technology have prompted a concern for a so-called “Correction.” While I can worry about the current gambling obsession spilling over to capital markets and distorting signals, theoretically, these AI stocks are valued in well-functioning markets by profit-maximizing buyers and sellers, based on expected cash flows and variability. Especially in today’s market, this variability can be significant, but it is reflected in prices.

While these periods in the stock market are comfortable, we must be cautious about extrapolating too far into the future.